Showing posts with label economics. Show all posts

Showing posts with label economics. Show all posts

Monday, May 30, 2022

Holiday Reading

Monarch butterflies bounce back in Mexico wintering groundsWhen I First Saw Elon Musk for Who He Really Is'Big Short' investor Michael Burry compares the market slump to a plane crash — and hints tumbling stocks and home sales remind him of the housing bubble burstingThe Southern Baptist Horror

Wednesday, December 23, 2020

Midweek Reading

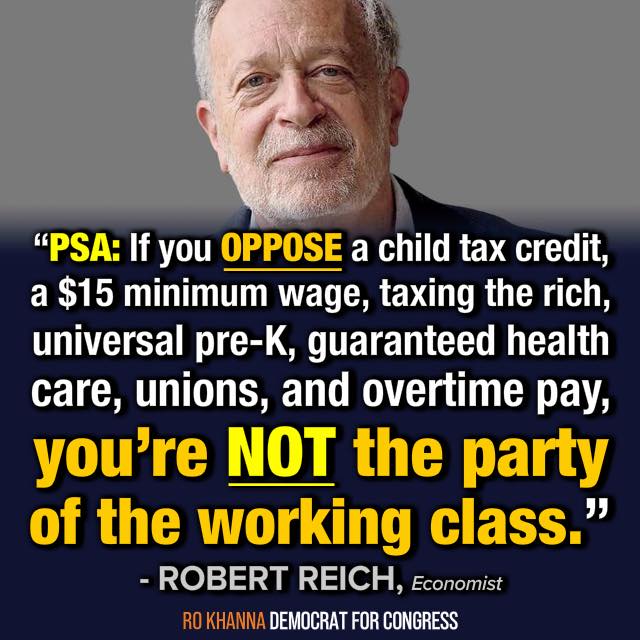

The Gadfly of American Plutocracy

How Compass Became the Bane of Real Estate

How One of the Reddest States Became the Nation’s Hottest Weed MarketWisconsin Supreme Court upholds Biden's win, rejects Trump lawsuitThe Election is Over. Wisconsin Turns to Redistricting.A new California bill would require a 4-year degree to become a copEverything We’ve Learned About Modern Economic Theory Is Wrong

How Compass Became the Bane of Real Estate

How One of the Reddest States Became the Nation’s Hottest Weed MarketWisconsin Supreme Court upholds Biden's win, rejects Trump lawsuitThe Election is Over. Wisconsin Turns to Redistricting.A new California bill would require a 4-year degree to become a copEverything We’ve Learned About Modern Economic Theory Is Wrong

Saturday, March 21, 2020

Friday, April 19, 2019

Weekend Reading

Why And How Capitalism Needs To Be Reformed

The IRS Tried To Take On The Ultrawealthy. It Didn't Go Well.

The Tax Law's Big Winner Is The Millionaire CEO

Bernie Sanders's Fox News Town Hall Wasn't A Debate. Bernie Won Anyway.

Warren Has A Good Beginning For Ending Corporate Tax Avoidance

The Truth About U.S. Taxes Is That They Aren't High Enough

Yes, Graceland Actually Threatened To Move To Japan To Get $194 Million In Subsidies From Memphis

Ending The Economic War Among The States: A Strategic Proposal

Amazon's Next Frontier: Your City's Purchasing

The Undemocratic Making Of Indianapolis

The Future Of Unions Is White-Collar

Fun Fictions In Economics

The IRS Tried To Take On The Ultrawealthy. It Didn't Go Well.

The Tax Law's Big Winner Is The Millionaire CEO

Bernie Sanders's Fox News Town Hall Wasn't A Debate. Bernie Won Anyway.

Warren Has A Good Beginning For Ending Corporate Tax Avoidance

The Truth About U.S. Taxes Is That They Aren't High Enough

Yes, Graceland Actually Threatened To Move To Japan To Get $194 Million In Subsidies From Memphis

Ending The Economic War Among The States: A Strategic Proposal

Amazon's Next Frontier: Your City's Purchasing

The Undemocratic Making Of Indianapolis

The Future Of Unions Is White-Collar

Fun Fictions In Economics

Friday, February 15, 2019

Talking Heads Upset Billionaire Isn't Given Billions In Corporate Welfare

Boo-fucking-hoo, you babies. Sorry your usual status-quo shakedown didn't work.

‘Morning Joe’ Rips Alexandria Ocasio-Cortez Over Amazon Pull-Out: ‘She Only Cares About Herself’

The set of “Morning Joe” was not happy about the decision by Amazon to pull out of their new planned headquarters in New York City yesterday, laying the blame for the decision at the feet of Rep. Alexandria Ocasio-Cortez and fellow recalcitrant progressive lawmakers.

On set there was near unanimity that Ocasio-Cortez did not understand the broader situation and was unfamiliar with basic economics.

“The protests that we saw were to get on AOC’s bandwagon. And what’s shocking to me is yet once again she shows how little she understands, about not just economics, but even unemployment,” show mainstay Susan Del Percio said. “Just because she has a progressive agenda, which some people like, does not mean she has the city’s best interests. What she showed me today, or yesterday, is that she only cares about herself.”Um, actually she understands the economics better than the Morning Joe corporate welfare shills.

How much was New York giving Amazon? What was the cost-per-job? If you're not going to discuss the details of the giveaway and actually analyze it in comparison to other possible investments, maybe you're the one who needs to shut the fuck up.

I guess, according to the Morning Joe crew, giving billions to a billionaire is good use of public dollars. Oh, but all these rich pricks hate socialism. Yeah, unless it's for them.

For Further Reading:

Amazon To Pay $0 In Federal Taxes In 2019

Economic Development, Tax Incentives and The Plutocracy It's Creating

Friday, July 6, 2018

Friday Reading

Is Foxconn Double Crossing Walker?

Unions Will Try To Thwart Supreme Court Janus Ruling - That's What They Did In Michigan

Meet The Economist Behind The One Percent's Stealth Takeover Of America

The Second Amendment's History

Is It Great To Be A Worker In The U.S.? Not Compared With The Rest Of The World

A 30-Year Alarm On The Reality Of Climate Change

Crude Oil Through Port Of Milwaukee Creates Risks For Lakefront, Water Supply

Business' Complaints Over Pressure For Donations Prompted Ouster of Ald. Tony Zielinski As Licenses Committee Head

No President Has Tied Themselves Closer To The Stock Market Than Trump - Now The Chickens Have Come Home To Roost

Scott Walker Is Donald Trumps Most Dangerous Enabler

Unions Will Try To Thwart Supreme Court Janus Ruling - That's What They Did In Michigan

Meet The Economist Behind The One Percent's Stealth Takeover Of America

The Second Amendment's History

Is It Great To Be A Worker In The U.S.? Not Compared With The Rest Of The World

A 30-Year Alarm On The Reality Of Climate Change

Crude Oil Through Port Of Milwaukee Creates Risks For Lakefront, Water Supply

Business' Complaints Over Pressure For Donations Prompted Ouster of Ald. Tony Zielinski As Licenses Committee Head

No President Has Tied Themselves Closer To The Stock Market Than Trump - Now The Chickens Have Come Home To Roost

Scott Walker Is Donald Trumps Most Dangerous Enabler

Sunday, July 16, 2017

Sunday Reading

Is Wisconsin Going to Get Fox-Conned?

Modern Economists:The Inept Firefighters' Clubs

Capitalism the Apple Way vs. Capitalism The Google Way

100 Companies Responsible For 71% Of Global Emissions

Scientists Starting To Clear Up One Of The Biggest Controversies In Climate Science

You Can Pay For A Ballpark Without Fleecing Taxpayers

The Fascinating Life Of Nikola Tesla

Walker Building Yesterday's Economy

Modern Economists:The Inept Firefighters' Clubs

Capitalism the Apple Way vs. Capitalism The Google Way

100 Companies Responsible For 71% Of Global Emissions

Scientists Starting To Clear Up One Of The Biggest Controversies In Climate Science

You Can Pay For A Ballpark Without Fleecing Taxpayers

The Fascinating Life Of Nikola Tesla

Walker Building Yesterday's Economy

Sunday, October 16, 2016

Weekend Reading

Scott Walker, the John Doe Files and How Corporate Cash Influences American Politics

How Privatization Is Killing The Public Sector

Scaring Kids About The National Debt

Wall Street Journal Mourns The Growing Efficiency of the Banking Industry

Elizabeth Warren Asks Obama To Replace Wall Street Regulator For Brazen Conduct

Ruling Against Wall Street Watchdog Decried As Reckless and Partisan

Oklahoma Governor Mary Fallin Declares 'Oilfield Prayer Day' To Ask God To Protect The State's Oil Industry

Larry Summers Makes The Case For Higher Capital Requirements

Social Security Is Not The Main Driver of the Country's Long-term Budget Problem

Economics Has A Major Blind Spot

Wisconsin Among The Worst Places In U.S. To Start A Business

Talgo Coming Back To Milwaukee

Solution To False 'Benefit Crisis' Isn't Cuts - It's Better Fiscal Policies

America Isn't The Greatest Country On Earth. It's No. 28

The Undercover War Against The Parks

How The Oil & Gas Industry Awakened Oklahoma's Sleeping Fault Lines

How Privatization Is Killing The Public Sector

Scaring Kids About The National Debt

Wall Street Journal Mourns The Growing Efficiency of the Banking Industry

Elizabeth Warren Asks Obama To Replace Wall Street Regulator For Brazen Conduct

Ruling Against Wall Street Watchdog Decried As Reckless and Partisan

Oklahoma Governor Mary Fallin Declares 'Oilfield Prayer Day' To Ask God To Protect The State's Oil Industry

Larry Summers Makes The Case For Higher Capital Requirements

Social Security Is Not The Main Driver of the Country's Long-term Budget Problem

Economics Has A Major Blind Spot

Wisconsin Among The Worst Places In U.S. To Start A Business

Talgo Coming Back To Milwaukee

Solution To False 'Benefit Crisis' Isn't Cuts - It's Better Fiscal Policies

America Isn't The Greatest Country On Earth. It's No. 28

The Undercover War Against The Parks

How The Oil & Gas Industry Awakened Oklahoma's Sleeping Fault Lines

Saturday, January 25, 2014

Weekend Reading

Oxfam Finds 85 Elites As Rich As 3.5 Billion People

Trickle-Down Economics Is The Greatest Broken Promise Of Our Lifetime

Here's Why The Idea Of A 'Traditional Marriage' Is Total Bullshit

25 Manners Everyone Needs

Health Care Spending Slows To Historically Low Rate

Income Growth Has Stalled For Most Americans

The Biggest Myths In Economics

No, Raising The Minimum Wage Won't Kill The Economy

8 Subconscious Mistakes Your Brain Makes Everyday

Trickle-Down Economics Is The Greatest Broken Promise Of Our Lifetime

Here's Why The Idea Of A 'Traditional Marriage' Is Total Bullshit

25 Manners Everyone Needs

Health Care Spending Slows To Historically Low Rate

Income Growth Has Stalled For Most Americans

The Biggest Myths In Economics

No, Raising The Minimum Wage Won't Kill The Economy

8 Subconscious Mistakes Your Brain Makes Everyday

Saturday, August 3, 2013

Income Inequality

Did Sprawl Kill Horatio Alger?

A Tale Of Two Rust Belt Cities

Will SCOTUS Voting Rights Ruling Yield A Blue State Refund?

Without State Spending There'd Be No Google Or GlaxoSmithKline

Econ 101 Is Killing America

McDonald's Budget Plan Leaves Out Corporate Welfare

The Case For Paying People More

Mr. President, Have Pity On The Working Man

How Intellectual Property Reinforces Inequality

Is Productivity Being Translated Into Pay Increases?

Higher Productivity Used To Mean Higher Wages. Has That Broken Down?

Wages Fall At Record Pace

Walmart One Of The Major Welfare Recipients In America

Who's Dependent On Food Stamps? Cheapskate Corporations

Inequality In America: The Data Is Sobering

A Tale Of Two Rust Belt Cities

Will SCOTUS Voting Rights Ruling Yield A Blue State Refund?

Without State Spending There'd Be No Google Or GlaxoSmithKline

Econ 101 Is Killing America

McDonald's Budget Plan Leaves Out Corporate Welfare

The Case For Paying People More

Mr. President, Have Pity On The Working Man

How Intellectual Property Reinforces Inequality

Is Productivity Being Translated Into Pay Increases?

Higher Productivity Used To Mean Higher Wages. Has That Broken Down?

Wages Fall At Record Pace

Walmart One Of The Major Welfare Recipients In America

Who's Dependent On Food Stamps? Cheapskate Corporations

Inequality In America: The Data Is Sobering

Saturday, August 11, 2012

Weekend Reading

Comparing Housing Recoveries

Five Myths About Obama's Stimulus

Giving Economics A Bad Name

Looks Like Ryan: Mitt's Pick

Obamacare Benefits Are Starting To Roll Out

The Opportunity Cost Of Hoarding Cash Is Lower Than You Think

Ryan Wants Even Bigger Tax Cuts For Wealthy Than Romney

Where The World's Running Out Of Water

Five Myths About Obama's Stimulus

Giving Economics A Bad Name

Looks Like Ryan: Mitt's Pick

Obamacare Benefits Are Starting To Roll Out

The Opportunity Cost Of Hoarding Cash Is Lower Than You Think

Ryan Wants Even Bigger Tax Cuts For Wealthy Than Romney

Where The World's Running Out Of Water

Friday, March 9, 2012

Weekend Reading

Monday, August 29, 2011

The End of Loser Liberalism

A new book from Dean Baker.

Contents

1 Upward Redistribution of Income ....... 1

2 Where We Are and How We Got Here........ 12

3 The Great Redistribution ......... 27

4 The Bubble Economy ............ 35

5 The Fed and Interest Rates........ 49

6 Full Employment without the Fed ....... 61

7 The Treasury and the Dollar ........ 79

8 Trade in an Overvalued-Dollar World...... 87

9 Reining in Finance.......... 111

10 Government-Granted Monopolies ..... 129

11 Follow the Money:......... 141

Sunday, October 11, 2009

Sunday Reading

ACORN: Federal Governments Best Investment

Affordable Housing Innovations

Economics of Models

Ending LEEDs Monopoly

High-Speed Rail: A No-Brainer

Midwest Has Highest Per Capita Rate of Iraq War Fatalities and Casualties

On Endless Growth

Owners No More

Perils of Waterfront Development

Private Equity Vultures

Problems With Securitization

Too Politically Connected To Fail In Any Crisis

Transport of Tomorrow

Whitopia

Affordable Housing Innovations

Economics of Models

Ending LEEDs Monopoly

High-Speed Rail: A No-Brainer

Midwest Has Highest Per Capita Rate of Iraq War Fatalities and Casualties

On Endless Growth

Owners No More

Perils of Waterfront Development

Private Equity Vultures

Problems With Securitization

Too Politically Connected To Fail In Any Crisis

Transport of Tomorrow

Whitopia

Monday, August 10, 2009

Economic Reform

Robert Skidelsky has an interesting article in the Financial Times concerning a reform of the economics profession.

Saturday, March 14, 2009

Unnecessary Economic Complications

You've got to love economic theories. Cute perfect-world scenarios wrapped up nicely in elegant algorithms. The problem is much of the assumptions are pure drivel.

I've always found that historical trend analysis seems to offer the most insight into where we've been and how to handle challenges presently and in the future. History is a wonderful guide in locating the norm (mean reversion) of whatever it is we're measuring. By just looking at how inflated the price-to-income and price-to-rent ratios had become towards the late 1990s, a few of our better economists were able to call the housing bubble back in 2002. They didn't have to dress-up the obvious in fancy mathematical models to show what was plain as day.

One particular Homo Economicus assumption I've seen popping up lately is the idea that people are averse to working more if they know it will lead them into a higher tax bracket. Of course this argument was brought out by conservatives as a warning against President Obama's plan to raise taxes on the wealthiest amongst us. [By the way, during our most robust period of growth from the late 40s to the late 60s our highest marginal tax rate varied from 90 to 70 percent.] It may be true that higher taxes lead millionaires to find more and more clever ways to avoid taxation, but regardless of the amount they are making, they always seem to be trying to avoid taxes. And, let's face it, can we really say many of these people are "working" that hard? Avoiding taxation isn't the same as doing less. This has more to do with profit and greed than some efficient decision about taxes and time worked.

This is especially true for the 85 percent of the population earning under $100,000. Most people work as much as they can for as long as they can. Which is why even though our productivity per hour has increased, so has our number of hours worked.

But I guess when our economic system is constructed toward rewarding the Haves every example displayed and the indicators used to explain what's going on will no doubt be more geared to their wealth -- the S&P, the Dow, Russell, Nasdaq, Goldman, etc. These have become the markers we all watch and live by. Yet the wealthiest control nearly all of the stock market. This misdirection is comparable to tracking sales at Neiman Marcus as a guide for the shopping patterns of average Americans.

I've always found that historical trend analysis seems to offer the most insight into where we've been and how to handle challenges presently and in the future. History is a wonderful guide in locating the norm (mean reversion) of whatever it is we're measuring. By just looking at how inflated the price-to-income and price-to-rent ratios had become towards the late 1990s, a few of our better economists were able to call the housing bubble back in 2002. They didn't have to dress-up the obvious in fancy mathematical models to show what was plain as day.

One particular Homo Economicus assumption I've seen popping up lately is the idea that people are averse to working more if they know it will lead them into a higher tax bracket. Of course this argument was brought out by conservatives as a warning against President Obama's plan to raise taxes on the wealthiest amongst us. [By the way, during our most robust period of growth from the late 40s to the late 60s our highest marginal tax rate varied from 90 to 70 percent.] It may be true that higher taxes lead millionaires to find more and more clever ways to avoid taxation, but regardless of the amount they are making, they always seem to be trying to avoid taxes. And, let's face it, can we really say many of these people are "working" that hard? Avoiding taxation isn't the same as doing less. This has more to do with profit and greed than some efficient decision about taxes and time worked.

This is especially true for the 85 percent of the population earning under $100,000. Most people work as much as they can for as long as they can. Which is why even though our productivity per hour has increased, so has our number of hours worked.

But I guess when our economic system is constructed toward rewarding the Haves every example displayed and the indicators used to explain what's going on will no doubt be more geared to their wealth -- the S&P, the Dow, Russell, Nasdaq, Goldman, etc. These have become the markers we all watch and live by. Yet the wealthiest control nearly all of the stock market. This misdirection is comparable to tracking sales at Neiman Marcus as a guide for the shopping patterns of average Americans.

Sunday, March 16, 2008

NAFTA & The Myth of Free Trade

John McCain recently indicated his position in the free trade debate and belittled his Democratic challengers by dismissing their reservations about and proposals of possible reform for the North American Free Trade Agreement (NAFTA). Yet, why should we trust McCain's judgment of NAFTA or anything closely resembling economics when he readily admits he doesn't understand the subject?

McCain went on to state, "The fundamentals of our economy are still strong." Huh? I think he's been on the campaign trail a bit too long. You don't have to have be an economics PhD to read the newspapers and grasp that our economy is headed in the wrong direction. Many parties and policies are to blame for this downturn. Reagan/Thatcher deregulation, lower taxation, and decreased protectionism; Greenspan/Rubin/Clinton continued deregulation, balanced budget obsession, and the dollar/stock/housing bubbles; and Bush's even lower taxation, deregulation, and costly and unnecessary war. So as we can see, there is a theme running through the last three decades and much of it is coming to a head.

In the 1980s we bailed out the savings & loan industry. Which, as Paul Krugman calculates, cost taxpayers 3.2 percent of GDP, or the equivalent of $450 billion today. Today, we're bailing out the cesspool that is the subprime mortgage industry. Both were caused by excessive deregulation and lack of oversight into the activities of what have become evermore-risky financial schemes. The U.S. has been on a steady path of lowering taxes on its corporations, tearing down trade restrictions (mostly to undercut labors' gains and their bargaining power), and removing any management and boundaries of standards of acceptable business practice. We're letting the foxes watch the hen house. All of this is done to please Wall Street-ers and to cook the books for acceptable quarterly returns for shareholders.

As Nouriel Roubini notes there now exists a shadow financial system, composed of conduits, money market funds, hedge funds and other non-bank financial institutions. "The Fed now can lend unlimited amounts to non-bank highly leveraged institutions that it does not regulate...By lending massive amounts to potentially insolvent institutions that it does not supervise or regulate and that may be insolvent the Fed is taking serious financial risks and seriously exacerbating moral hazard."

We've entered into an era of uber casino capitalism where rules and ethics no longer apply. Aided by bought-and-paid-for government policies, elite capital plunders and pillages the globe in search of higher returns. This is all claimed under the guise of creating jobs, advancing democracy, increasing wages, and advancing civilization. Yet all of these assertions are empirically and demonstrably false.

Alice Amsden, an MIT economist, has demonstrated that most of the successful Asian nations have violated every aspect of the law of comparative advantage on their path to economic success. Ha-Joon Chang, a Cambridge economist, has shown that almost all countries have used protectionist measures to protect their infant industries and to develop economically throughout time. Unadulterated free trade, virtually non-existent taxes, and the lack of any protectionist measures, as an economic development policy is a modern scheme. This is a ruse that is failing miserably. Developed countries grew at 3.2 percent during the 1960-1980 period. Their growth stalled to just 2.2 percent, from 1980-2000. Over this same time, developing countries growth decreased from 3 percent to 1.5 percent.

Alexander Hamilton, America's first treasury secretary, proposed measures to protect America's infant industries. Since 1791, up until the Second World War, the U.S economy grew behind huge tariff walls, with industrial tariffs ranging from 25 to 40 percent. Direct government participation and protection of industry resulted in the economic strength and maturity of the nation. "Within 200 years, when America has gotten out of protection all that it can offer, it too will adopt free trade," Ulysses Grant (civil war hero, U.S. president 1868-1876) commenting on U.S. trade policy with parallels to England's history of protection and their change in attitude to free trade when they saw that they had gotten all that protection could offer them.

The countries that have accomplished economic ascendancy have done so by fashioning policies to their own needs, not by following neo-liberal orthodoxy (aka The Washington Consensus). Today, China and India have tariffs ranging between 20 and 30 percent on manufactured goods. The productivity gap between rich (developed) and poor (developing) countries is much higher today than it was, so it only follows that tariffs should also be higher. The ratio of per capita income in purchasing power parity between the richest and poorest developed countries was, at most, four-to-one. Today the gap is around fifty-to-one. Today's developing countries will have to impose higher tariff rates than those used by developing countries in the past if they are to provide the actual same degree of protection to their industries. Infant economies cannot compete with mature ones. Free trade agreements between countries with vastly different levels of productivity cannot succeed over the long-term.

From 1993 (NAFTA's inception) to 2002, the U.S. lost 879,280 jobs due to the trade agreement. Wisconsin has lost 23,028 jobs due to NAFTA over this period. Productivity has risen by 48 percent since 1973, yet real hourly compensation has increase by only 20 percent. In 1973 manufacturing accounted for 24 percent of total U.S. employment, it is now only roughly 10 percent. Trade liberalization has been most hurtful to those without college degrees, whom have actually seen their wages decline.

The neoliberal experiment has failed. It's time for a new New Deal. Imagine that -- government restricting corrupt financial practices and putting the people back to work, whilst also initiating some new programs, legislation, and policies aimed at benefiting the majority of the population rather than a select monied few. As Stanley Kutler's recent article states, "The New Deal launched vast public works projects, expanding and improving the nation's infrastructure...More than eight million people working on one million projects, benefited from the program. The Roosevelt administrations enduring legacy came from its reform measures...the Social Security Act...legislation and regulatory commissions for banking, securities, communications, and labor practices." If only we hadn't spent the last three decades tearing apart these policies and legislation, much of today's horrible financial news and depressing economic conditions could have been averted.

And this also ties into immigration, obviously. First, although this is free trade and is supposed to be based on Ricardo's comparative advantage, which is supposed to lead to efficiency and productivity gains. But with the U.S. continually subsidizing farmers, we artificially lower the price of American agricultural exports and hurt developing countries. Such as Mexico, in one area where they can actually produce at a lower cost. Instead, our subsidized agri-business drives Mexican farmers off their land because of our low priced agricultural products. And, because of this, Mexican wages have actually fallen since NAFTA. Hmmm, I wonder where they might go to find better wages?

For Further Reading:

Challenging Neoliberal Myths

Consensus Against Neoliberal Washington Consensus

Economics of Empire

Fair Trade

False Promises on Trade

How the Washington Consensus Endangers U.S. National Security

Myth of Free Trade

NAFTA at Ten: The Recount

Post-Washington Dissensus

Rethinking Global Political Economy

Subprime Bailout Bonanza

McCain went on to state, "The fundamentals of our economy are still strong." Huh? I think he's been on the campaign trail a bit too long. You don't have to have be an economics PhD to read the newspapers and grasp that our economy is headed in the wrong direction. Many parties and policies are to blame for this downturn. Reagan/Thatcher deregulation, lower taxation, and decreased protectionism; Greenspan/Rubin/Clinton continued deregulation, balanced budget obsession, and the dollar/stock/housing bubbles; and Bush's even lower taxation, deregulation, and costly and unnecessary war. So as we can see, there is a theme running through the last three decades and much of it is coming to a head.

In the 1980s we bailed out the savings & loan industry. Which, as Paul Krugman calculates, cost taxpayers 3.2 percent of GDP, or the equivalent of $450 billion today. Today, we're bailing out the cesspool that is the subprime mortgage industry. Both were caused by excessive deregulation and lack of oversight into the activities of what have become evermore-risky financial schemes. The U.S. has been on a steady path of lowering taxes on its corporations, tearing down trade restrictions (mostly to undercut labors' gains and their bargaining power), and removing any management and boundaries of standards of acceptable business practice. We're letting the foxes watch the hen house. All of this is done to please Wall Street-ers and to cook the books for acceptable quarterly returns for shareholders.

As Nouriel Roubini notes there now exists a shadow financial system, composed of conduits, money market funds, hedge funds and other non-bank financial institutions. "The Fed now can lend unlimited amounts to non-bank highly leveraged institutions that it does not regulate...By lending massive amounts to potentially insolvent institutions that it does not supervise or regulate and that may be insolvent the Fed is taking serious financial risks and seriously exacerbating moral hazard."

We've entered into an era of uber casino capitalism where rules and ethics no longer apply. Aided by bought-and-paid-for government policies, elite capital plunders and pillages the globe in search of higher returns. This is all claimed under the guise of creating jobs, advancing democracy, increasing wages, and advancing civilization. Yet all of these assertions are empirically and demonstrably false.

Alice Amsden, an MIT economist, has demonstrated that most of the successful Asian nations have violated every aspect of the law of comparative advantage on their path to economic success. Ha-Joon Chang, a Cambridge economist, has shown that almost all countries have used protectionist measures to protect their infant industries and to develop economically throughout time. Unadulterated free trade, virtually non-existent taxes, and the lack of any protectionist measures, as an economic development policy is a modern scheme. This is a ruse that is failing miserably. Developed countries grew at 3.2 percent during the 1960-1980 period. Their growth stalled to just 2.2 percent, from 1980-2000. Over this same time, developing countries growth decreased from 3 percent to 1.5 percent.

Alexander Hamilton, America's first treasury secretary, proposed measures to protect America's infant industries. Since 1791, up until the Second World War, the U.S economy grew behind huge tariff walls, with industrial tariffs ranging from 25 to 40 percent. Direct government participation and protection of industry resulted in the economic strength and maturity of the nation. "Within 200 years, when America has gotten out of protection all that it can offer, it too will adopt free trade," Ulysses Grant (civil war hero, U.S. president 1868-1876) commenting on U.S. trade policy with parallels to England's history of protection and their change in attitude to free trade when they saw that they had gotten all that protection could offer them.

The countries that have accomplished economic ascendancy have done so by fashioning policies to their own needs, not by following neo-liberal orthodoxy (aka The Washington Consensus). Today, China and India have tariffs ranging between 20 and 30 percent on manufactured goods. The productivity gap between rich (developed) and poor (developing) countries is much higher today than it was, so it only follows that tariffs should also be higher. The ratio of per capita income in purchasing power parity between the richest and poorest developed countries was, at most, four-to-one. Today the gap is around fifty-to-one. Today's developing countries will have to impose higher tariff rates than those used by developing countries in the past if they are to provide the actual same degree of protection to their industries. Infant economies cannot compete with mature ones. Free trade agreements between countries with vastly different levels of productivity cannot succeed over the long-term.

From 1993 (NAFTA's inception) to 2002, the U.S. lost 879,280 jobs due to the trade agreement. Wisconsin has lost 23,028 jobs due to NAFTA over this period. Productivity has risen by 48 percent since 1973, yet real hourly compensation has increase by only 20 percent. In 1973 manufacturing accounted for 24 percent of total U.S. employment, it is now only roughly 10 percent. Trade liberalization has been most hurtful to those without college degrees, whom have actually seen their wages decline.

The neoliberal experiment has failed. It's time for a new New Deal. Imagine that -- government restricting corrupt financial practices and putting the people back to work, whilst also initiating some new programs, legislation, and policies aimed at benefiting the majority of the population rather than a select monied few. As Stanley Kutler's recent article states, "The New Deal launched vast public works projects, expanding and improving the nation's infrastructure...More than eight million people working on one million projects, benefited from the program. The Roosevelt administrations enduring legacy came from its reform measures...the Social Security Act...legislation and regulatory commissions for banking, securities, communications, and labor practices." If only we hadn't spent the last three decades tearing apart these policies and legislation, much of today's horrible financial news and depressing economic conditions could have been averted.

And this also ties into immigration, obviously. First, although this is free trade and is supposed to be based on Ricardo's comparative advantage, which is supposed to lead to efficiency and productivity gains. But with the U.S. continually subsidizing farmers, we artificially lower the price of American agricultural exports and hurt developing countries. Such as Mexico, in one area where they can actually produce at a lower cost. Instead, our subsidized agri-business drives Mexican farmers off their land because of our low priced agricultural products. And, because of this, Mexican wages have actually fallen since NAFTA. Hmmm, I wonder where they might go to find better wages?

For Further Reading:

Challenging Neoliberal Myths

Consensus Against Neoliberal Washington Consensus

Economics of Empire

Fair Trade

False Promises on Trade

How the Washington Consensus Endangers U.S. National Security

Myth of Free Trade

NAFTA at Ten: The Recount

Post-Washington Dissensus

Rethinking Global Political Economy

Subprime Bailout Bonanza

Subscribe to:

Comments (Atom)